Raise your home

As a registered participant, you may be eligible for funding to raise your home above the assessed flood level and 2021-2022 flood event level.

Your Home Assessment Report will indicate if this is recommended for your home. Check your Home Assessment Report to learn more.

Home raising might not be suitable for everyone, and you should take your personal circumstances into consideration, including accessibility. If home raising isn’t for you, you may be eligible for the Resilient Retrofit program.

IMPORTANT: Registrations of interest for the Resilient Homes Fund including the Home Raising program closed on 30 July 2023.

If you plan to sell your home, all building works and payments need to be finalised before the settlement date. You cannot transfer your registration to another person. When the financial settlement of your home sale occurs, your registration will be withdrawn.

Homeowners who are registered in the Fund and still own the property, are eligible to apply for funding through Queensland Rural and Industry Development Authority (QRIDA). Grant applications can be submitted until 1 December 2025. All approved building works must be completed and paid in full to the licensed contractor by 30 June 2026.

Eligibility

In addition to the standard eligibility requirements for the Resilient Homes Fund, your home must:

- have been inundated by floodwaters above the habitable floor level from one of the eligible 2021-2022 weather events.

- be practical to raise, ideally timber-framed and clad homes (single or double brick, or slab-on-ground homes are often not practical or cost effective to raise).

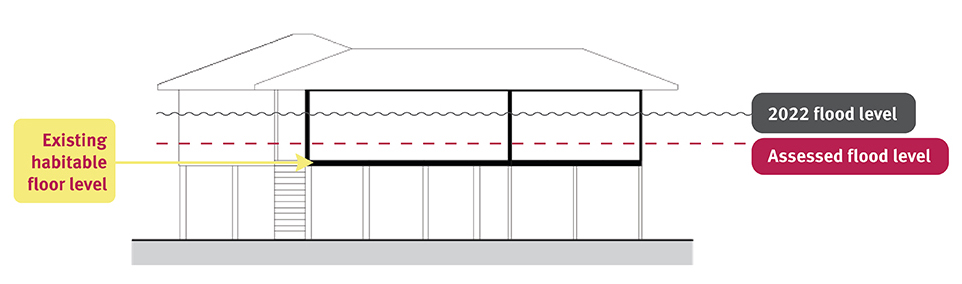

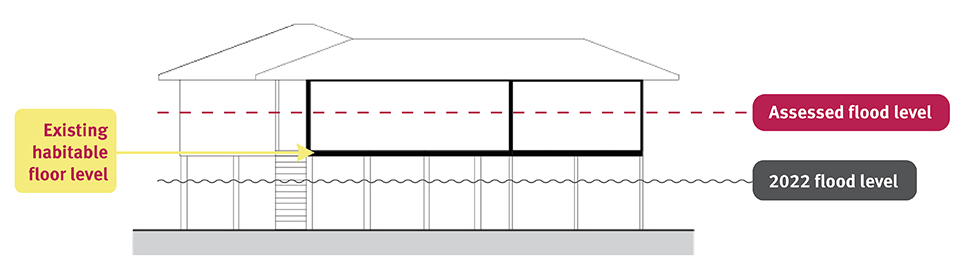

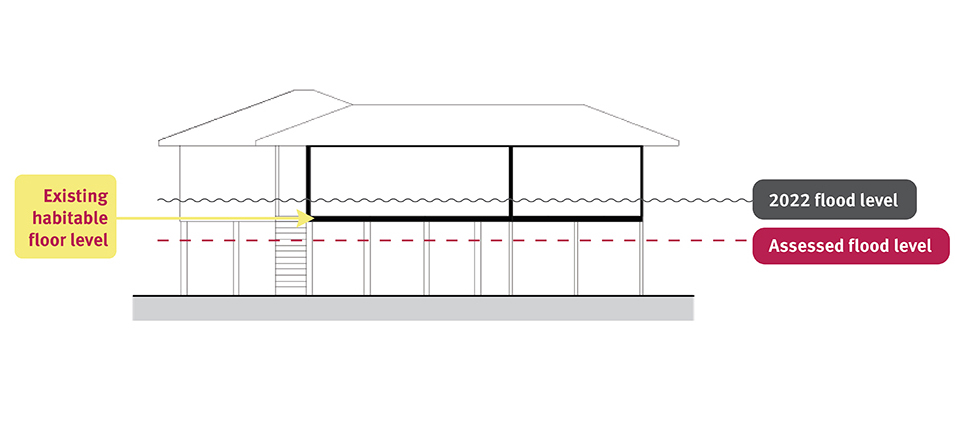

- have a habitable floor level below the assessed flood level and the 2021-2022 flood event level as specified by your local council.

We recently expanded the Home Raising program eligibility criteria to support more homeowners to raise their homes.

Assessed flood level

We provide an assessed flood level in your Home Assessment Report (if it's available when we prepared your report) to help you understand whether your current habitable floor level is below or above the recommended (assessed) level.

The assessed flood level is the minimum level you should build resilience to and is based on the minimum habitable floor level specified by your local council.

Homes built above the minimum assessed flood level are less likely to experience frequent flooding. It does not represent a historical flood level and it is possible that flood levels could exceed this level in the future.

We recommend you contact your local council to get more flood information for your property and local area so that you can better understand your flood risk and prepare for future flooding.

Preliminary works

After you've been notified that you're eligible for the Home Raising program, you have some additional steps to take before funding can be approved. This is because your local council may have restrictions around home raising.

To meet these requirements, you need to seek council approval and complete preliminary works. Read more about arranging home-raising preliminary works.

Available funding

You can apply for up to $150,000 towards the cost of home raising.

If the habitable floor level of your home is below both the assessed flood level and the 2021-2022 flood event level, you will also be eligible for a dollar-for-dollar co-contribution from the Home Raising program for any costs over $150,000. Find out more about co-contributions.

If the habitable floor level of your home is below either the assessed floor level or the 2021-2022 flood event level, no co-contribution is available (the maximum funding you can apply for is $150,000).

You can only receive funding under one program. That means you cannot apply for Home Raising program and the Resilient Retrofit program.

If your Home Assessment Report recommends multiple options, you should assess the benefits and risks, timing and costs, and your personal circumstances to choose which option is best for you.

You can use available funding for:

- soil tests and hydraulic reports

- site survey (stormwater, sewer, gas etc.)

- professional services (associated engineering drawings, architectural/drafting fee, certifier fees)

- relocating and reconnecting of essential services

- reinstating existing stairs for access (and constructing additional stairs where safety requirements were not met by existing access)

- building approval fees and development application fees (where required)

- minimal, to code requirements for sub-surface ground control such as grading/placement of gravel on the ground under the newly raised house and creation or connection of stormwater gully to existing home stormwater line

- post-raise floor level survey

- development/building application fees and relevant permits related to the works (e.g. footpath closure permits if required)

- minor structural damage associated with the usual raise process required to deliver a minimal viable product

- removal of asbestos at risk of being disturbed or to facilitate access for raising

- minimal earthworks to facilitate access for raising

- electrical works required to meet minimum building certification.

Generally, the fund will not cover the following costs:

- a concrete slab

- decks or other extensions to the existing floor area or building footprint

- reinstating decks that must be removed to facilitate the home raise

- façade/finishing items such as slats

- accommodation during construction

- driveway construction/repairs

- reinstating any major structural damage that is the result of poor workmanship during house raise

- internal refurbishment works not required for raising (waterproofing, plumbing, and glazing)

- reinstating any floor space (including for example enclosed rooms or decks) that must be removed to facilitate the house raise

- earthworks not required for raise landscaping.

Required outcome

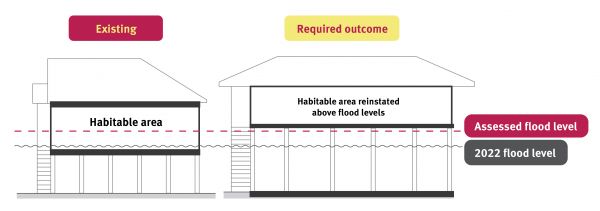

Single storey home on stumps – example A

The home is already on stumps, where the habitable area is both below the 2021-2022 flood event level and the assessed flood level. To be eligible for funding, the home must be raised to be at or above whichever level is higher.

In this example, the homeowner would receive base funding of $150,000 plus a dollar-for-dollar co-contribution for any costs over this amount. If the habitable area for this home had been below the assessed flood level but above the 2021-2022 flood event level (or vice versa), the homeowner could still receive funding to raise the home above the higher of the two levels, however funding would be capped at $150,000.

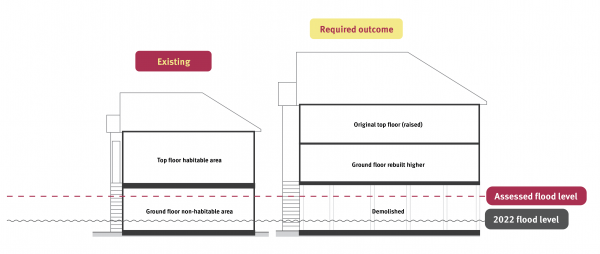

Two storey home raise – example B

The lower level of the existing home is raised above the assessed flood level and the 2021-2022 flood event level. The new lowest level of the home is not enclosed or converted into a new habitable area.

This homeowner can apply for up to $150,000. Co-contributions are not available, as this home is not considered practical to raise.

If home raising isn’t an option, an eligible homeowner could instead decide to demolish and relocate part of their home as an extension, as long as the total floor area is not increased.

Building under a raised home

We strongly recommend not building in (enclosing) the lower level of your raised home to use it as a habitable area (such as a bedroom or living room).

Doing so will reduce your home’s resilience and increase your risk of significant impact in future flooding events including:

- Increased flood vulnerability: Enclosing the area will trap the water and cause damage to the building and contents. It can also prevent your home from adequately drying out, contributing to mould issues and maintenance costs.

- Affects structural integrity: Your home raise design and the original foundation of the home may not account for the increased load, leading to stability issues. Obstructing floodwaters and flood debris can also affect the structural integrity of your home.

- Safety hazards: Water levels can rise rapidly and pose a threat to individuals residing in the lower levels of a raised home. If escape routes become inaccessible due to flooding, it can put occupants at risk of being trapped.

- Insurance and regulatory limitations: Insurers and regulatory authorities may have specific restrictions for building in flood-prone areas. They often have stringent requirements, especially if your home was raised under the Resilient Homes Fund. If you do not comply you can have insurance issues and difficulties getting necessary permits. You may also be subject to penalties or be required to demolish or remove built-in areas that have not been approved.